Executive View | SACCO Digitisation, Growth, and Regulatory Agility

SACCO STRATEGY | GEN Z | DIGITAL TRANSFORMATION | MOBILE-FIRST GROWTH

Future-Proofing SACCOS: Why Digitising for Gen Z Is Now a Survival Strategy

The strongest SACCOs in the next decade will not simply be the ones with the most branches or the oldest brands. They will be the ones that make joining, saving, borrowing, and getting support feel natural on the phone in a member’s hand.

For SACCO CEOs, boards, CIOs, COOs, regulators, cooperative leaders, and digitisation teams | Research-informed editorial | May 2026

The strategic point is simple:

The biggest risk is no longer changing platforms. The biggest risk is waiting while the next generation builds financial habits somewhere else.

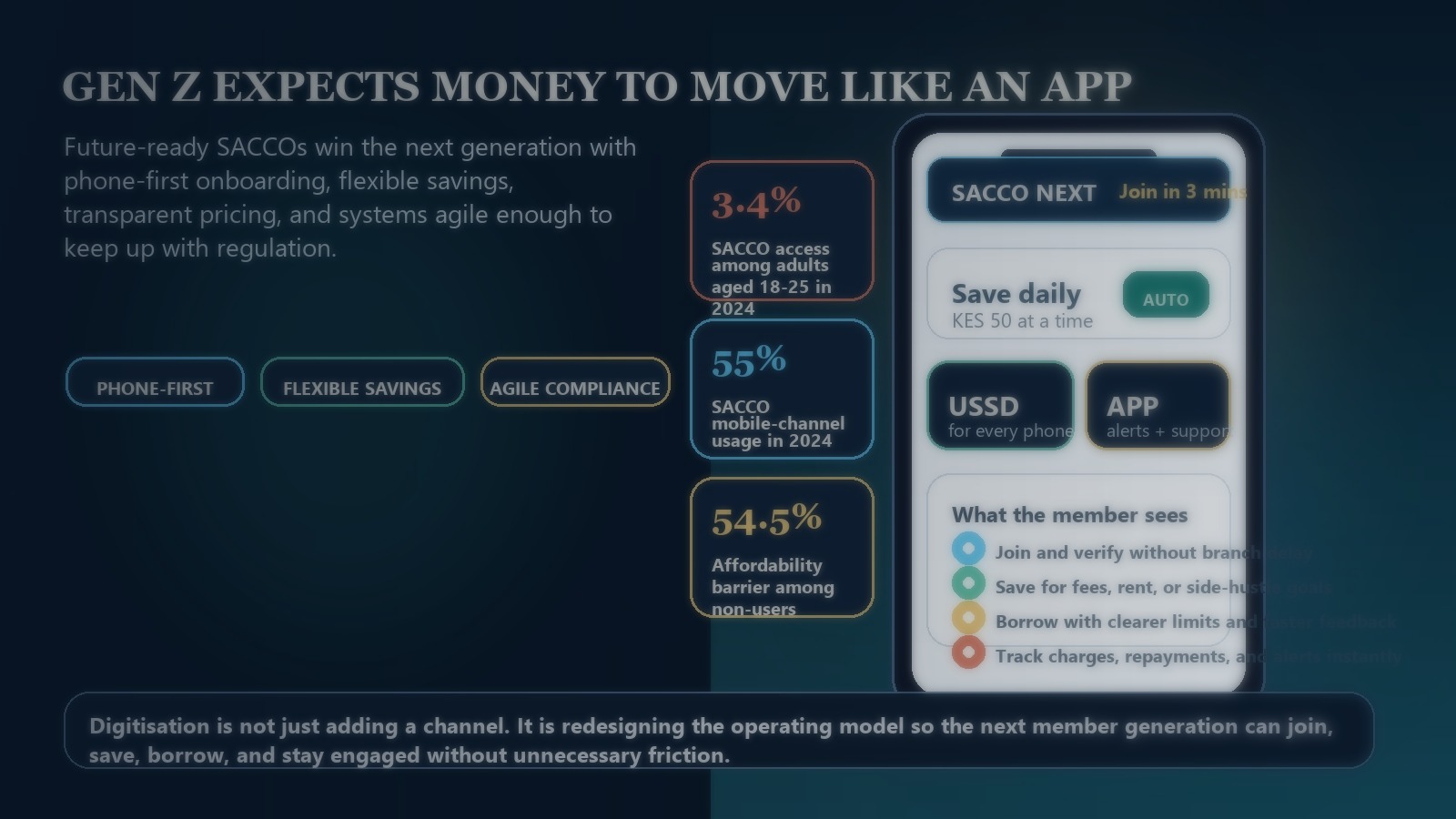

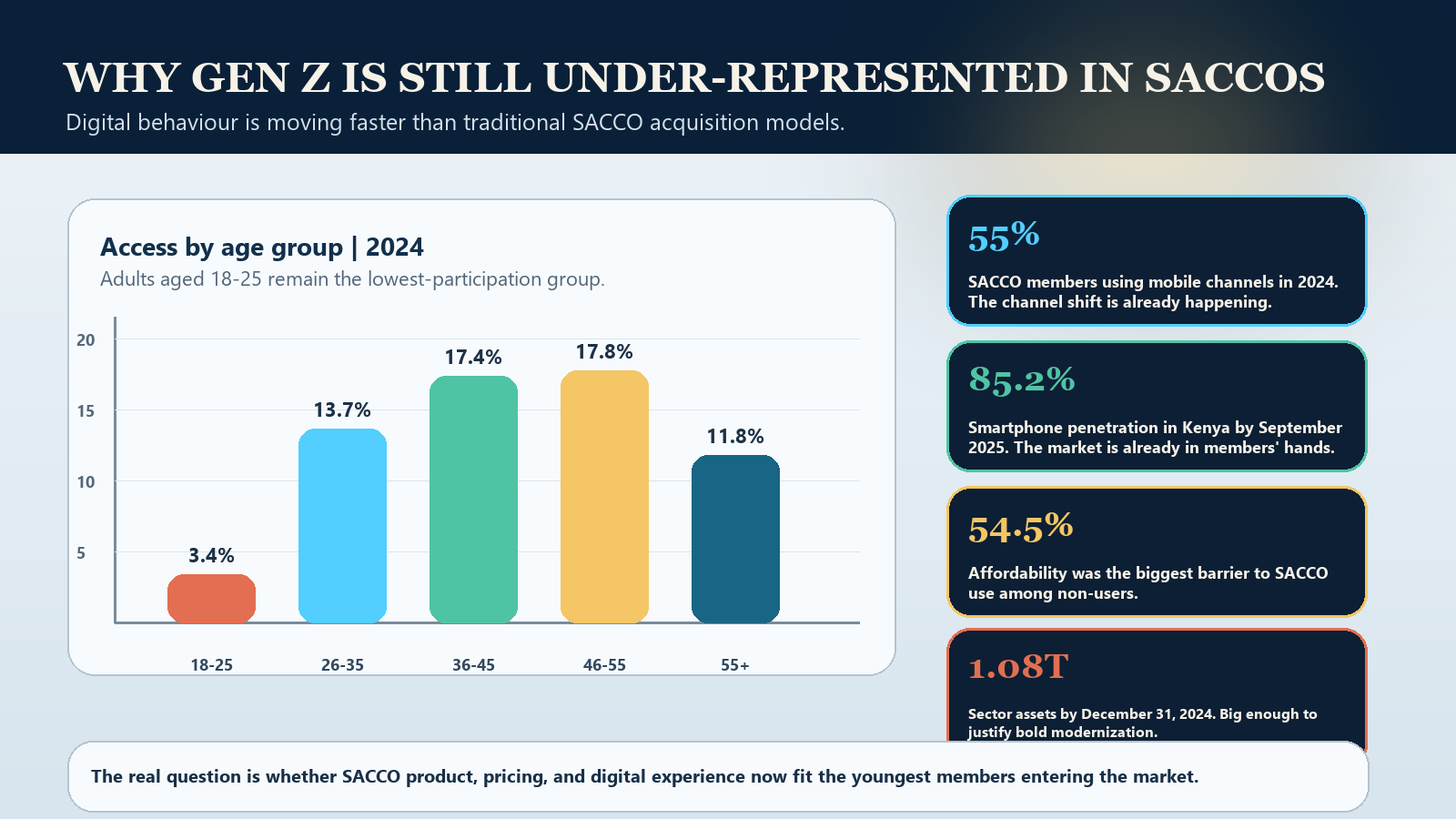

Kenya’s regulated SACCO sector remains large and important, with 356 regulated SACCOs, KSh 1.08 trillion in assets, and 7.39 million members by December 31, 2024. But the youngest adult cohort is still the weakest-linked segment. Adults aged 18-25 recorded only 3.4 percent SACCO access in 2024, even as SACCO mobile-channel usage rose sharply and the wider Kenyan market continued moving deeper into phone-led finance.

That is the warning. The sector is growing, but youth adoption is not keeping pace with digital behavior. Future-proofing therefore requires more than a website refresh or a new app icon. It requires product redesign, channel redesign, workflow redesign, and systems that can respond faster to customer expectations and regulatory change.

Gen Z Is Already Mobile-First

Kenya’s market is already phone-led, with strong smartphone and mobile money penetration. SACCOs must show up in that reality.

Youth Participation Is Still Low

The youngest adult cohort is the least represented in SACCO access, which means growth and relevance are both at stake.

Affordability And Eligibility Still Block Entry

Products built for stable salaries and branch routines still exclude many younger and informal-income members before they even start.

1. Digitisation is now a survival issue, not a side project.

SACCOs do not compete only with other SACCOs anymore. They compete with mobile money habits, bank apps, digital lenders, super-app expectations, and a generation that has learned to judge service by speed, clarity, and convenience. Once that behavior is formed elsewhere, it becomes expensive to win back.

The opportunity cost of delay therefore compounds quietly. It appears as lower youth acquisition, weaker fee growth, thinner member activity, fewer digital data signals, slower product iteration, and reduced relevance in the segment that should become tomorrow’s loyal base. A platform change may feel risky, but irrelevance is more dangerous.

2. To attract Gen Z, SACCOs have to be where their customers already are.

That means more than launching an app. It means designing the full service model around the devices, channels, and rhythms that younger members already use. For some members, that will be a smartphone app. For others, it will still be USSD. The point is not to force one channel. The point is to make entry, usage, and support possible without unnecessary friction.

Gen Z does not compare a SACCO only with another cooperative. They compare it with the easiest digital experience they had this week. If fees are unclear, onboarding is slow, support disappears, balances update late, or small savings are treated as unimportant, the product feels behind the market even if the institution itself is financially sound.

What Gen Z usually expects from a financial service

- Fast onboarding with less paperwork and clearer next steps.

- Transparent charges before money moves, not after.

- Flexible small-balance saving that respects irregular income.

- Real-time alerts and visibility on deposits, repayments, and fees.

- Self-service plus responsive support through the same digital channel.

- Products that feel relevant to real life such as school fees, rent, small business, or side-hustle savings goals.

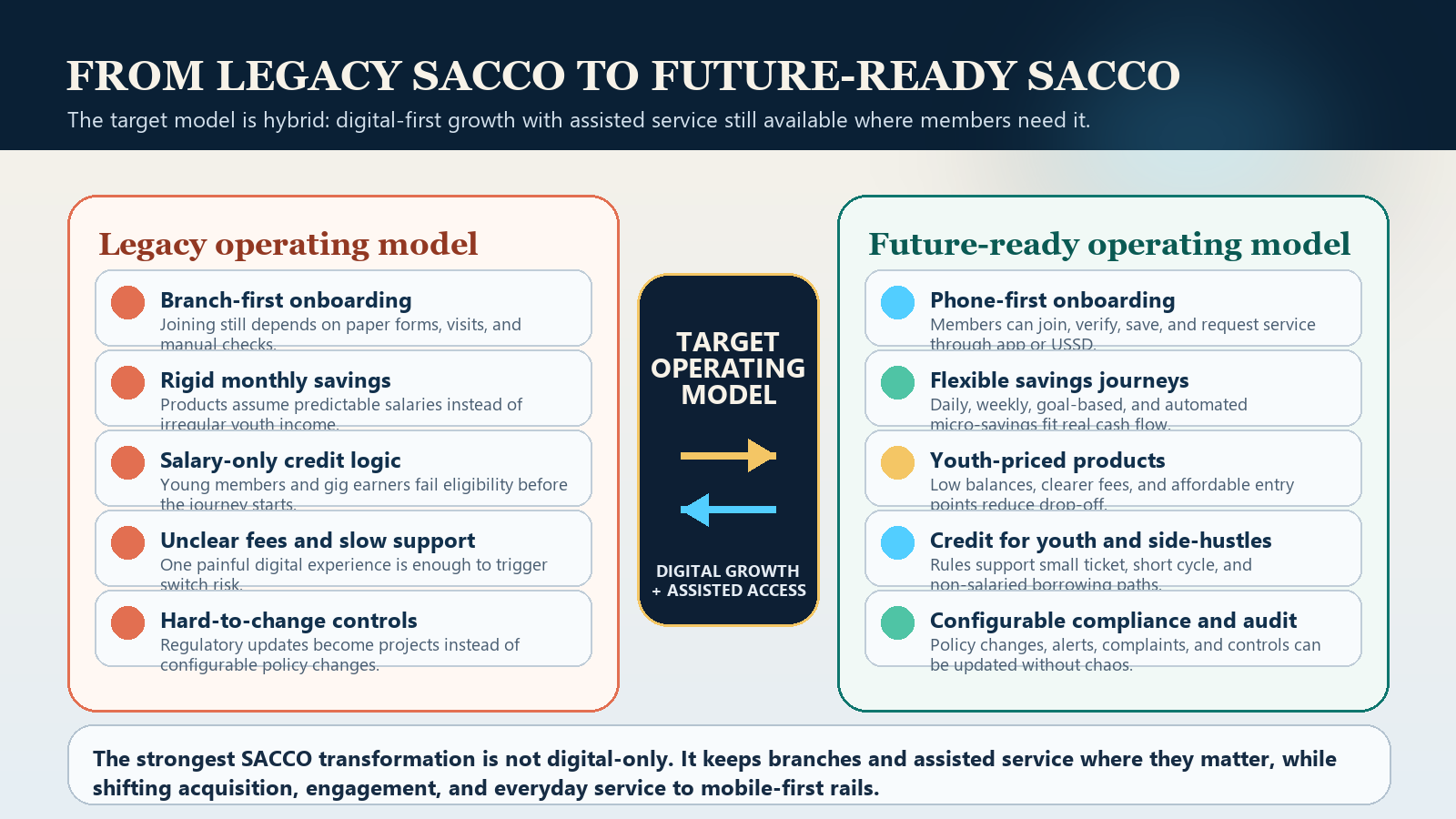

3. Old ways of working will not survive the competition.

Many SACCO processes still assume a familiar but narrowing member profile: salaried, branch-comfortable, patient with manual checks, and willing to accept rigid monthly contribution routines. That is no longer a safe default. A younger market includes students, side-hustlers, freelancers, informal workers, creators, first-job earners, and members whose cash flow does not arrive in a predictable monthly pattern.

When products are built around regular payroll deductions, guarantor-heavy entry, and slow branch loops, younger members experience the institution as restrictive before they experience it as helpful. That weakens not only acquisition but also the perception of relevance.

The future-ready SACCO does not ask young members to adapt to old structures. It redesigns the structure to fit real member behavior.

4. What a future-ready SACCO should change now

- Build phone-first onboarding. Let members join, verify identity, activate accounts, and start using the SACCO without treating the branch as the mandatory first step.

- Offer flexible savings journeys. Daily, weekly, goal-based, and automated micro-savings work better for younger and irregular-income members than one rigid monthly model.

- Create youth-priced entry products. Low minimum balances, cleaner fees, and simple product language lower the emotional and financial cost of first adoption.

- Rethink credit for non-salaried members. Small-ticket lending, simpler qualification paths, alternative repayment rails, and transparent eligibility logic matter if youth are to see SACCO credit as usable.

- Make digital service dependable, not decorative. A bad first experience, repeated downtime, or confusing transaction flow can push a young member out faster than a branch campaign can bring them in.

- Add practical financial wellness tools. Budget prompts, savings goals, fee visibility, reminders, and self-service support make SACCOs more useful in everyday life, not just at loan time.

5. Regulatory change now demands agility, not just compliance effort.

SACCO digitisation is no longer only a customer experience conversation. It is also a governance, consumer protection, and operational resilience conversation. As supervisory expectations continue to evolve around complaints handling, consumer protection, data privacy, cybersecurity, AML, audit visibility, and responsible service delivery, rigid systems become expensive to maintain.

That means the real question is not simply whether a SACCO has software. The real question is whether its platform can adapt quickly when rules, products, thresholds, workflows, approvals, or reporting requirements change. The institutions that can configure faster, monitor cleaner, and audit better will respond with less disruption and lower compliance stress.

Systems capabilities that matter more over time

- Configurable rules and workflows instead of hard-coded product behaviour.

- Clear audit trails across users, approvals, changes, and exceptions.

- Complaint and service visibility so issues can be tracked before they erode trust.

- Stronger digital channel monitoring so downtime and friction are seen quickly and explained clearly.

- API and integration readiness so new rails, partners, and channels do not become risky improvisations.

6. The right model is hybrid, not digital-only.

Future-proofing does not mean abandoning members who still prefer traditional access. Older and rural members may continue to rely more heavily on assisted and branch-based service, even while younger and urban members move decisively toward mobile channels. That is why the strongest operating model is hybrid.

In practical terms, that means preserving trusted assisted channels while shifting acquisition, lightweight service, alerts, statements, small savings, and routine transactions to digital rails. This protects inclusion while still allowing the SACCO to grow where the market is moving fastest.

Keep

Trusted branches, assisted onboarding where needed, relationship-led service, and human support for complex journeys.

Shift

Joining, alerts, goal savings, statements, simple payments, small-ticket lending, and everyday engagement to app and USSD channels.

Strengthen

Core workflows, audit controls, complaints visibility, partner integration discipline, and reporting readiness for faster regulatory response.

7. The executive takeaway

Digitising for Gen Z is not a branding exercise. It is a survival strategy. The SACCOs that win will be the ones that lower friction, reduce member effort, fit irregular income realities, respond faster to regulatory change, and make digital service feel dependable enough for daily use.

That is the real future-proofing question: not whether a SACCO can launch a digital channel, but whether it can redesign itself so the next generation actually wants to stay.

Data note

This article draws on public findings from the 2024 FinAccess Household Survey, the FSD Kenya SACCO Subsector Report, Communications Authority of Kenya sector statistics, Deloitte banking research on younger digital consumers, and SASRA public regulatory materials.

Where Apex fits in this shift

A modern SACCO platform should support flexible savings, digital onboarding, mobile and USSD channels, lending workflows, audit trails, reporting visibility, and configuration agility. That is where Apex Softwares positions its core banking and digital finance stack for institutions that want to modernise without losing control.