Kenya’s Digital Lenders Need More Than a Loan App

The next winners in digital lending will not be built on disconnected tools. They will be built on real lending infrastructure.

Core Banking

Mobile

Agency

Web

M-Pesa

Business Intelligence

licensed digital credit providers in Kenya as of April 2026.

loans issued by licensed DCPs as of February 2026.

loan value already processed by licensed digital lenders.

Kenya’s digital lending market has moved beyond experimentation. As of April 2026, the Central Bank of Kenya had licensed 227 digital credit providers, and by February 2026 licensed providers had already issued 7.5 million loans valued at KSh 133.5 billion. This is now a regulated, scaling and highly competitive sector.

The question is no longer whether digital lending works. The real question is this: what kind of system does a serious digital lender need in order to grow safely, efficiently and profitably?

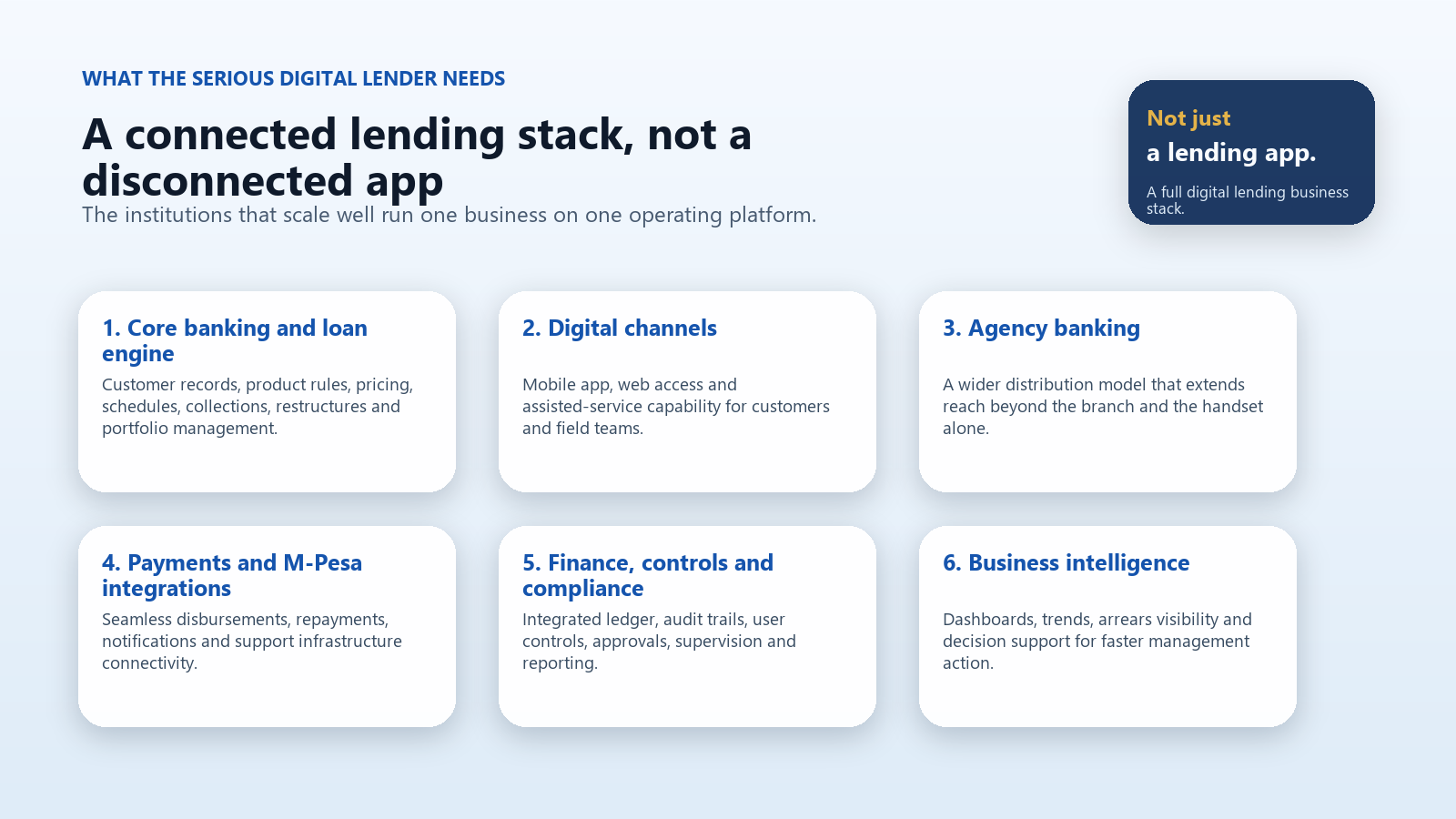

What the market actually needs

To scale well, digital lenders need a system stack that supports the entire business, not just the customer-facing moment of disbursement.

Customer records, product rules, pricing, loan books, repayments, restructures and portfolio quality management.

Approval logic, automated decision paths, maker-checker controls and internal supervision.

Mobile, web and agency channels that widen reach and support customers in the way they actually transact.

Payments, notifications, KYC flows, scoring, collections and external service connectivity.

Integrated ledger, audit trails, user controls, reporting and stronger governance as the book grows.

Dashboards, portfolio visibility and early warning insight so management can act before small issues become structural problems.

Why this matters now

Too many institutions still think digital lending is just a front-end app, an M-Pesa disbursement connection and a collections workflow. That is not a lending business. That is a channel.

A real digital lender needs a full operating platform behind the product. Without that, scale creates operational risk, reconciliation pain, weak control and fragmented customer data.

The Apex position

At Apex, that is exactly what we are offering. We provide a full suite built for growth: core banking, mobile, agency banking and web, with seamless integrations to M-Pesa and other supporting infrastructure.

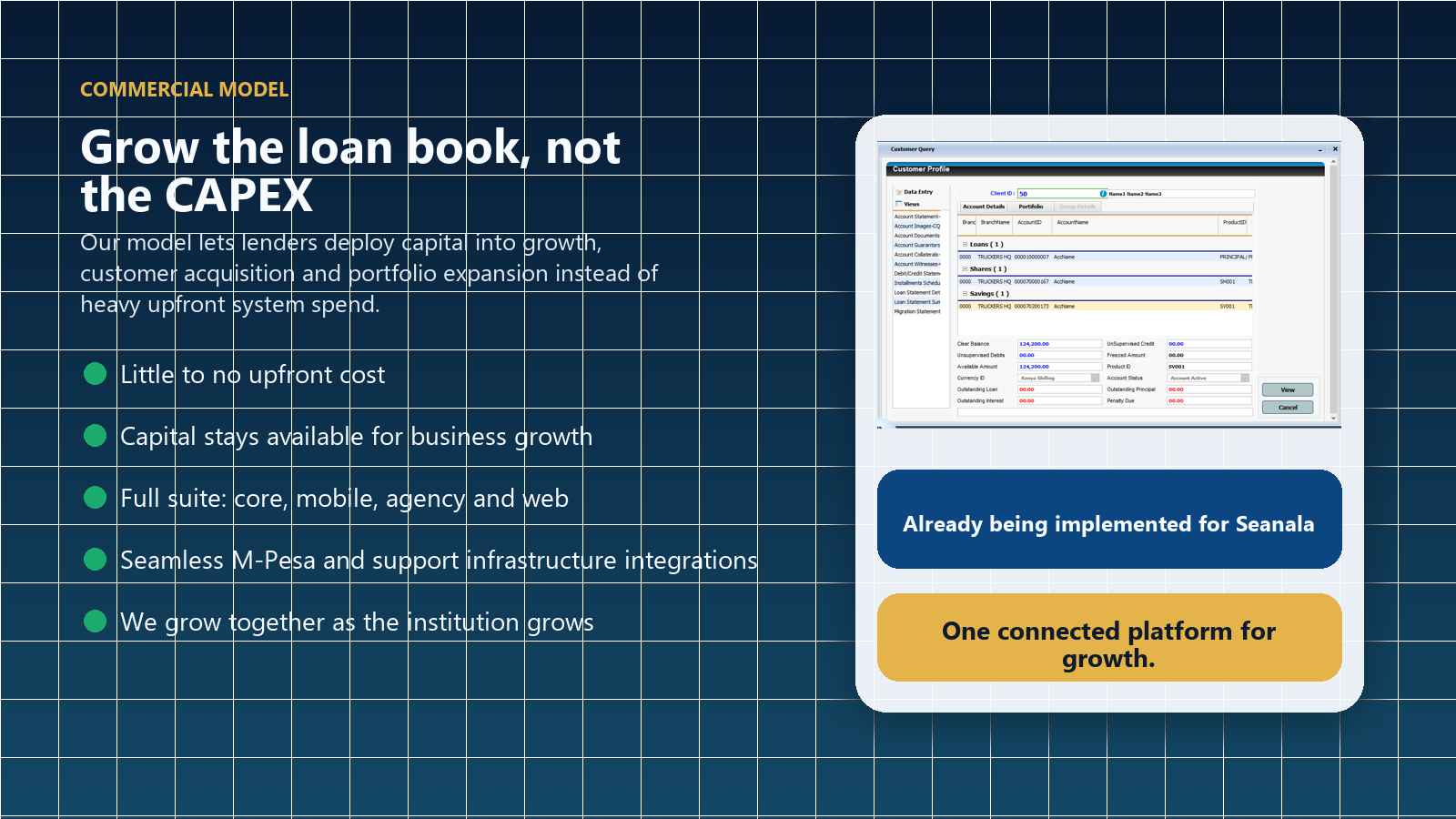

It is designed for institutions that want to move from lending activity to lending scale. We believe digital lenders should use their capital to grow the business, build their book and deepen market reach instead of locking scarce capital into heavy software acquisition costs upfront.

That is why we are offering this suite with little to no upfront cost, allowing institutions to direct capital into growth while still accessing the systems they need to operate professionally.

Proof in motion

This is not theory. We are already implementing this suite for Seanala, including a full core banking platform, mobile capability, agency capability and web access, together with the integrations needed to support real operations.

- Full core banking platform

- Mobile capability

- Agency capability

- Web access

- Seamless M-Pesa and support infrastructure integrations

- Little to no upfront cost model

One connected platform for digital lending growth

Kenya’s licensed digital lending market is growing fast. The next competitive edge will come from platform quality, operational control and distribution strength.

That is the platform we are building. And that is the partnership we are offering.

Use capital for growth

Scale with operational control

Grow together with the business

Leave a Comment