Executive View | Core Banking Leadership

Your Core Is Costing More Than You Think

Why many banks underestimate the true economic drag of legacy core banking systems, and why the biggest cost is often not what appears in the IT budget.

For CIOs, CEOs, CTOs, and senior banking decision-makers | April 2026 | Editorial feature

Most banks know what their core banking platform costs to license, host, support, and maintain. Fewer know what it costs them in slower product launches, manual workarounds, delayed integrations, change-related risk, and management time. That is the real problem. The visible cost of a core is usually manageable. The hidden cost is what compounds quietly across the institution.

The direct cost is on the budget. The indirect cost is buried in operations, delivery delays, and missed growth.

The system may still be running. That does not mean it is running economically.

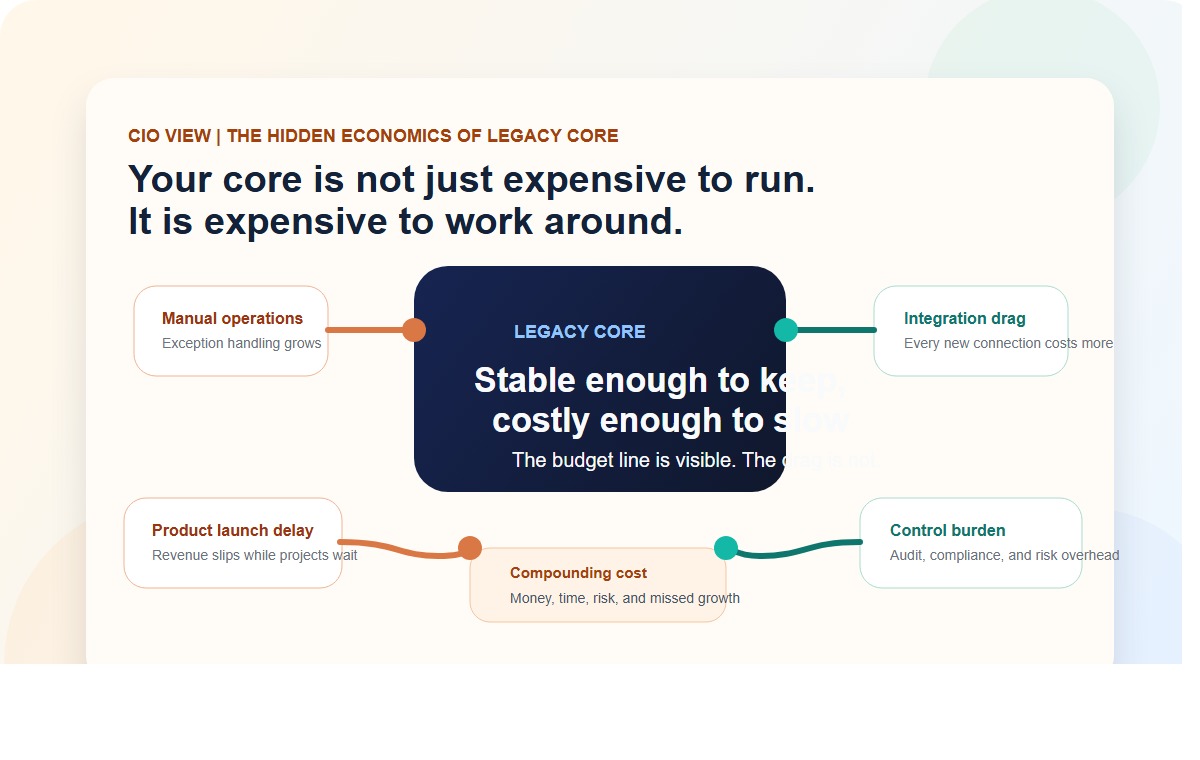

The bank keeps paying for the same core twice. Once to keep it alive, and again to work around its limits.

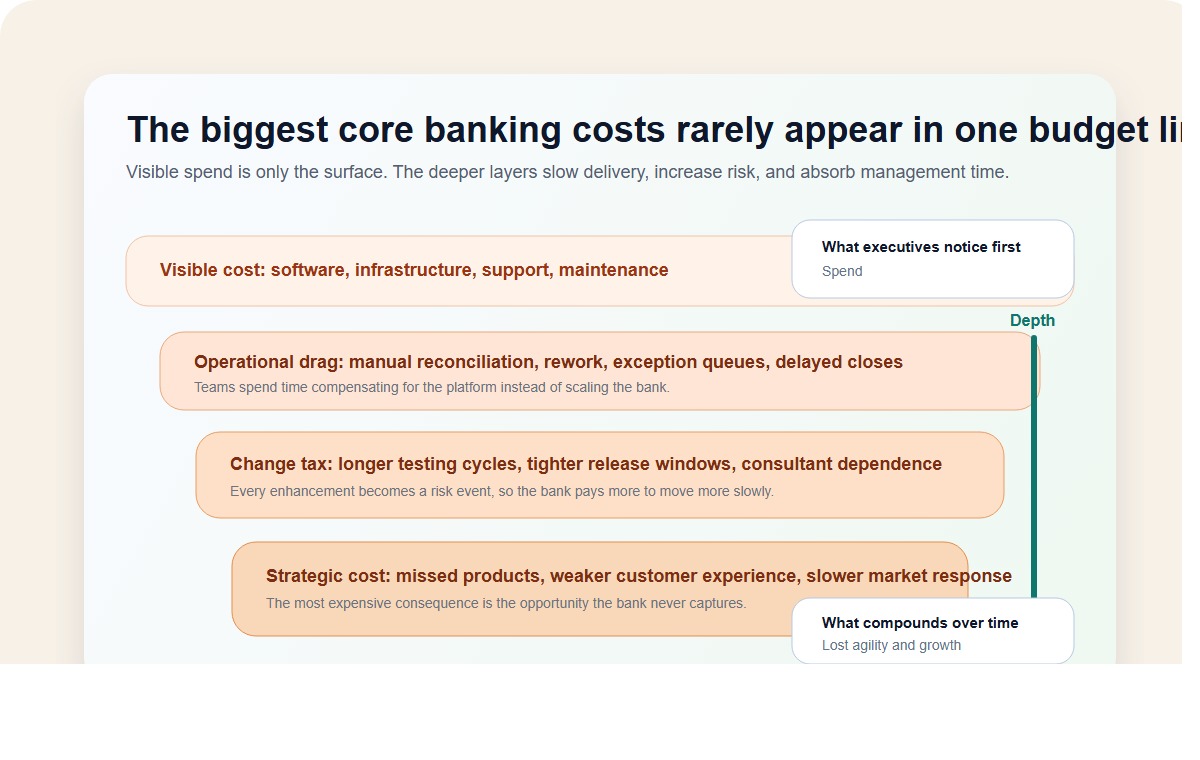

1. The software bill is only the surface

When executives discuss core banking costs, the conversation usually starts with licenses, infrastructure, support contracts, and upgrade projects. Those are real costs, but they are not the full economics of the platform. A legacy core can impose a second layer of cost that is far more difficult to measure: operational drag.

Operational drag appears when staff spend too much time on reconciliation, exception handling, reporting workarounds, interface fixes, release coordination, and post-change monitoring. None of those activities look like core licensing. All of them exist because the platform is harder to change and harder to trust than it should be.

That is why a platform that seems affordable on paper can be expensive in practice. The bank is not just funding a system. It is funding the friction around the system.

2. Every workaround becomes a permanent tax

Workarounds are rarely temporary in banking. Once a manual process, parallel spreadsheet, special integration, or custom exception route becomes part of daily operations, it tends to stay. Teams adapt around the core because the institution has to keep moving. Over time, those workarounds accumulate into a permanent operating tax.

A bank may discover that what once looked like system stability is actually organizational compensation. Operations teams absorb missing flexibility. Technology teams absorb integration complexity. Risk and control functions absorb additional oversight work. Product teams absorb slower launch timelines. The bank keeps functioning, but at a much higher internal cost than leaders intended.

This is where legacy cores become particularly misleading. They appear to support the business because the institution has built layers of human effort around them. Remove that human effort, and the true cost structure becomes obvious.

3. The hidden cost stack is deeper than most boards see

The biggest financial problem with an aging core is not usually one catastrophic failure. It is the accumulation of many smaller costs that deepen over time. The bank pays first in direct spend, then in operational inefficiency, then in slower change, and finally in strategic opportunity cost.

That final layer matters most. If it takes too long to configure products, onboard partners, expose APIs, launch digital features, or respond to regulatory change, the bank loses momentum. In highly competitive markets, lost momentum is lost revenue.

4. Slow product delivery is a revenue problem, not just an IT problem

Many banks still frame core modernization as a technology efficiency exercise. That is too narrow. If the platform makes it difficult to introduce new savings products, lending variants, pricing models, digital journeys, or embedded finance partnerships, the bank is paying an innovation penalty.

This is where CIOs and business leaders need sharper alignment. The cost of a legacy core is not only what the technology function spends to maintain it. It is also what the commercial side cannot do fast enough because the platform imposes too much release friction. A missed quarter in product delivery can be more expensive than a year of infrastructure savings.

In other words, core banking cost should not be measured only in expense terms. It should be measured in time-to-market, product flexibility, and ability to scale without multiplying operational overhead.

5. Control and compliance overhead also rise when the core is opaque

Another hidden cost comes from poor operational visibility. When platforms are difficult to interpret, the bank compensates with additional oversight, longer testing cycles, heavier approvals, and more manual evidence gathering. That increases the cost of audit, risk management, and compliance operations.

A modern core should reduce that burden. It should surface service health, workflow status, interface failures, reconciliation exceptions, configuration changes, and audit signals in ways teams can act on quickly. When the system explains itself clearly, the institution spends less time proving control and more time exercising it effectively.

What the bank is really paying for

- Money: direct software, infrastructure, support, and customization costs.

- Time: slower releases, longer testing, delayed product delivery, and slower integration cycles.

- Risk: fragile changes, more operational workarounds, and higher control overhead.

- Opportunity: products not launched, markets not reached, partnerships not activated, and customers not retained.

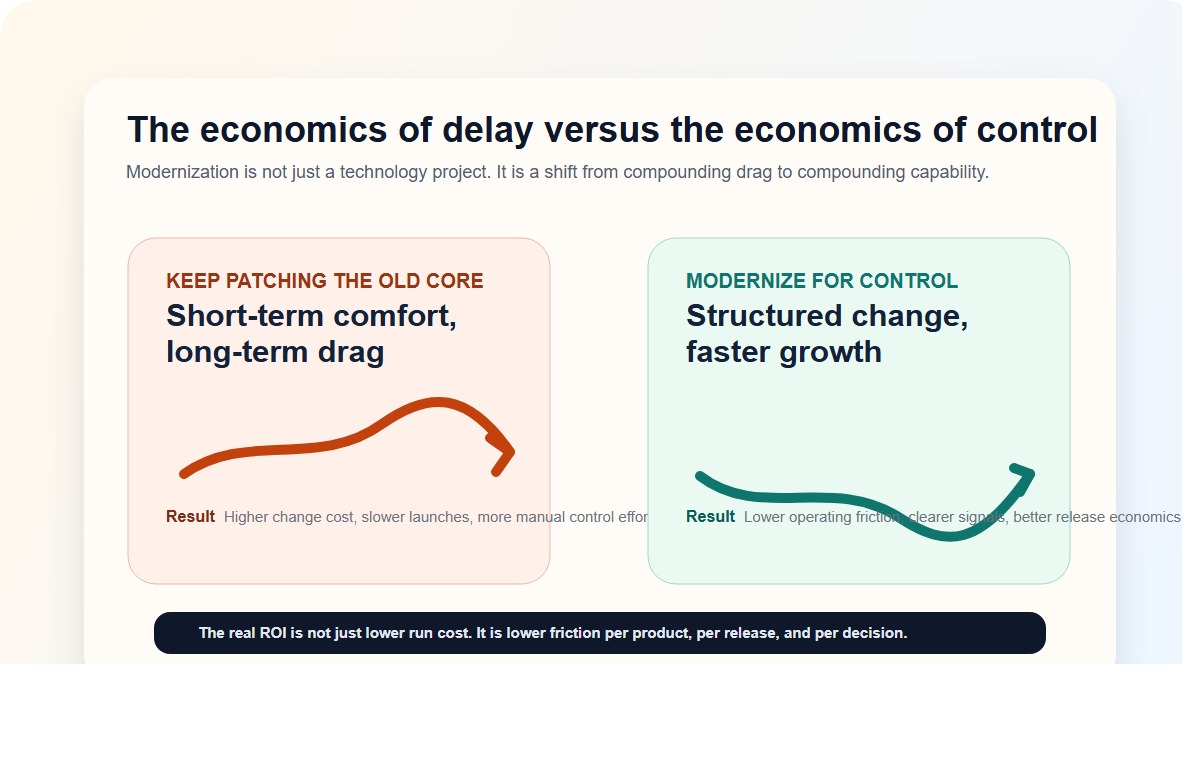

6. The case for modernization is economic discipline

Banks do not modernize their core because modernization sounds ambitious. They modernize because continuing to operate through mounting friction is a poor economic choice. The strongest case for a better core is not theatrical transformation. It is lower friction per release, lower dependency on workarounds, lower operating cost per product, and higher confidence in scale.

That is why the most credible providers should position modern core banking as a control and growth platform. The right architecture helps the institution launch faster, integrate more cleanly, manage risk more intelligently, and operate with fewer compensating processes. That is a much stronger value proposition than feature volume alone.

7. What executives should demand from the next core

If a bank is going to invest in core renewal, it should demand more than technical modernization language. The platform should make the business cheaper to run and easier to grow. That means modular architecture, stronger observability, explicit integration governance, flexible product configuration, and clearer operational signals for management, technology, and control teams alike.

The right question is no longer, “What does the core cost us?” It is, “What is the bank paying because the core is difficult to change?” That question leads to better technology decisions and better commercial outcomes.

The executive takeaway

Your core banking system is costing more than you think when the institution must compensate for it through manual operations, slower launches, heavier controls, and expensive change cycles. The banks that gain advantage will be the ones that evaluate core platforms not only by run cost, but by how much friction they remove from the business.

Image notes

- Hero visual: local JPG showing how hidden cost radiates out from a legacy core.

- Cost stack visual: local JPG showing the layered economics of direct and indirect core costs.

- Modernization economics visual: local JPG comparing the cost curve of delay versus structured modernization.