Success Story | Digital Wallet and Agency Banking

ETHIOPIA | WALLET | AGENT OPERATIONS | INTEROPERABILITY

How Plutus turned a digital wallet ambition for Ethiopia into a real rollout story.

The success was not that a wallet idea sounded compelling. The success was that the hardest part had already been built: customer journeys, agent operations, back-office control, USSD support, and an interoperability-ready architecture working together on one shared platform.

For Ethiopian banks and MFIs, that changes the conversation from “can this be built?” to “how quickly can this be hardened, integrated, and piloted?”

Why this matters:

A serious digital finance programme becomes easier to approve when the institution is not being asked to fund discovery twice.

Plutus already carried enough delivery value to move directly into hardening, integration planning, pilot readiness, and rollout control. That is what made it a success story: the foundation was real, the operating model was visible, and the remaining work was disciplined execution rather than speculative invention.

1. The problem was not the lack of a vision. It was the risk of starting from zero.

Ethiopian digital finance programmes usually carry two pressures at once. On one side, institutions want growth: more customers, more transactions, more convenience, more inclusion, and more digital reach. On the other side, they need control: KYC, operational authority, branch visibility, audit evidence, and a credible path into ecosystem integration.

Too many wallet discussions fail because they begin with a generic concept and a long delivery promise. That creates a familiar executive problem: the strategy sounds attractive, but the path to a real controlled rollout still feels distant. Plutus solved that by starting much further ahead.

Growth pressure

Institutions need a platform that can support onboarding, payments, savings, lending, and service expansion without years of delay.

Control pressure

Executives need proof that digital convenience will still sit inside an institution-grade control model.

Delivery pressure

Leadership teams are more likely to move when the highest-risk build work has already been materially completed.

2. Plutus succeeded because it already looked like a real operating platform.

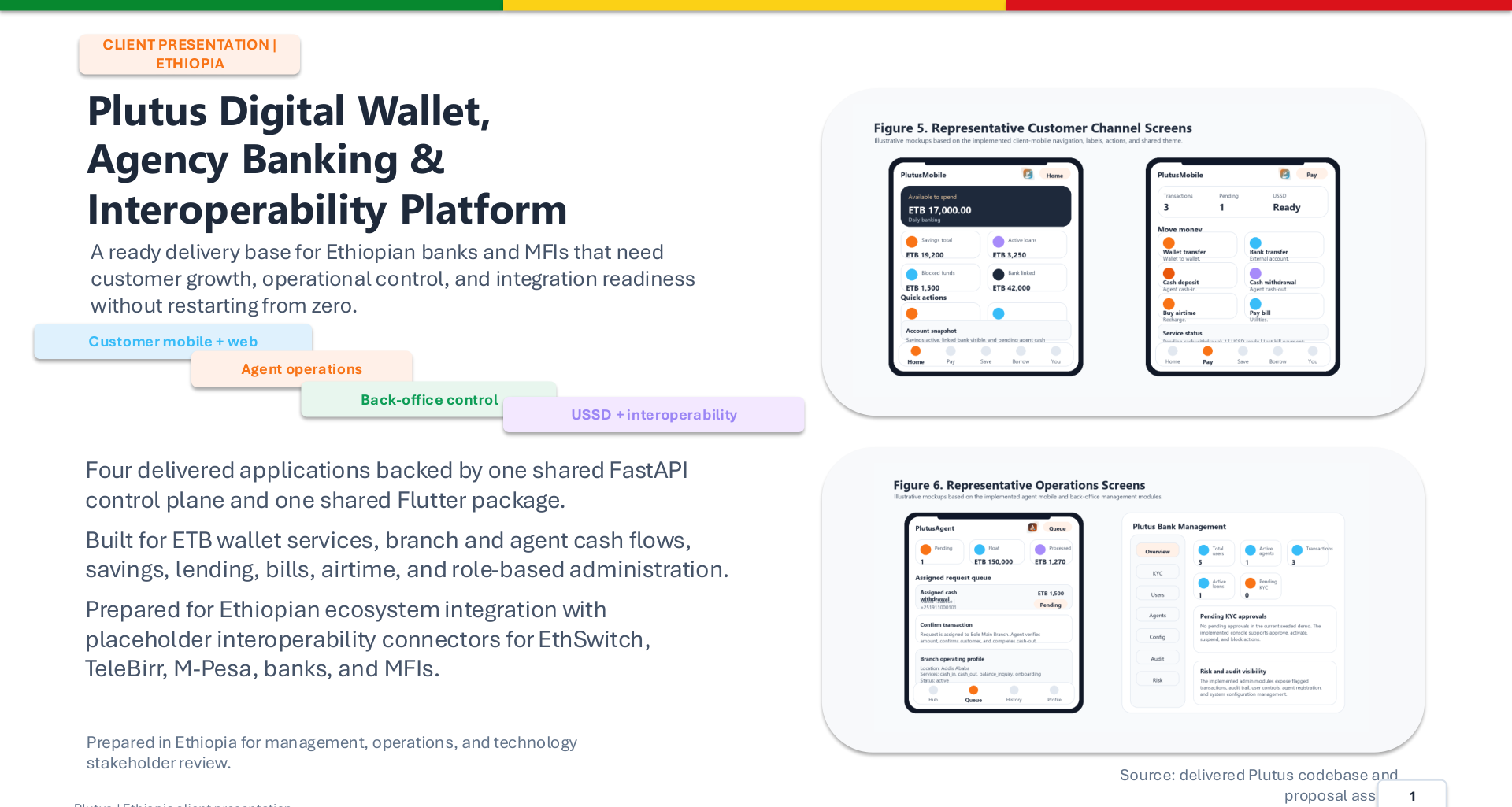

What made the platform credible was not one feature. It was the shape of the whole solution. Customer mobile and web journeys existed. Agent cash-service workflows existed. A management console existed. USSD existed. The backend rules engine was shared. The architecture already pointed toward interoperability, not just a closed-loop demo.

That meant the story was immediately stronger in executive discussions. Instead of asking a client to imagine what might be possible after months of development, Plutus could show how the institution would actually operate across channels, roles, and transaction types.

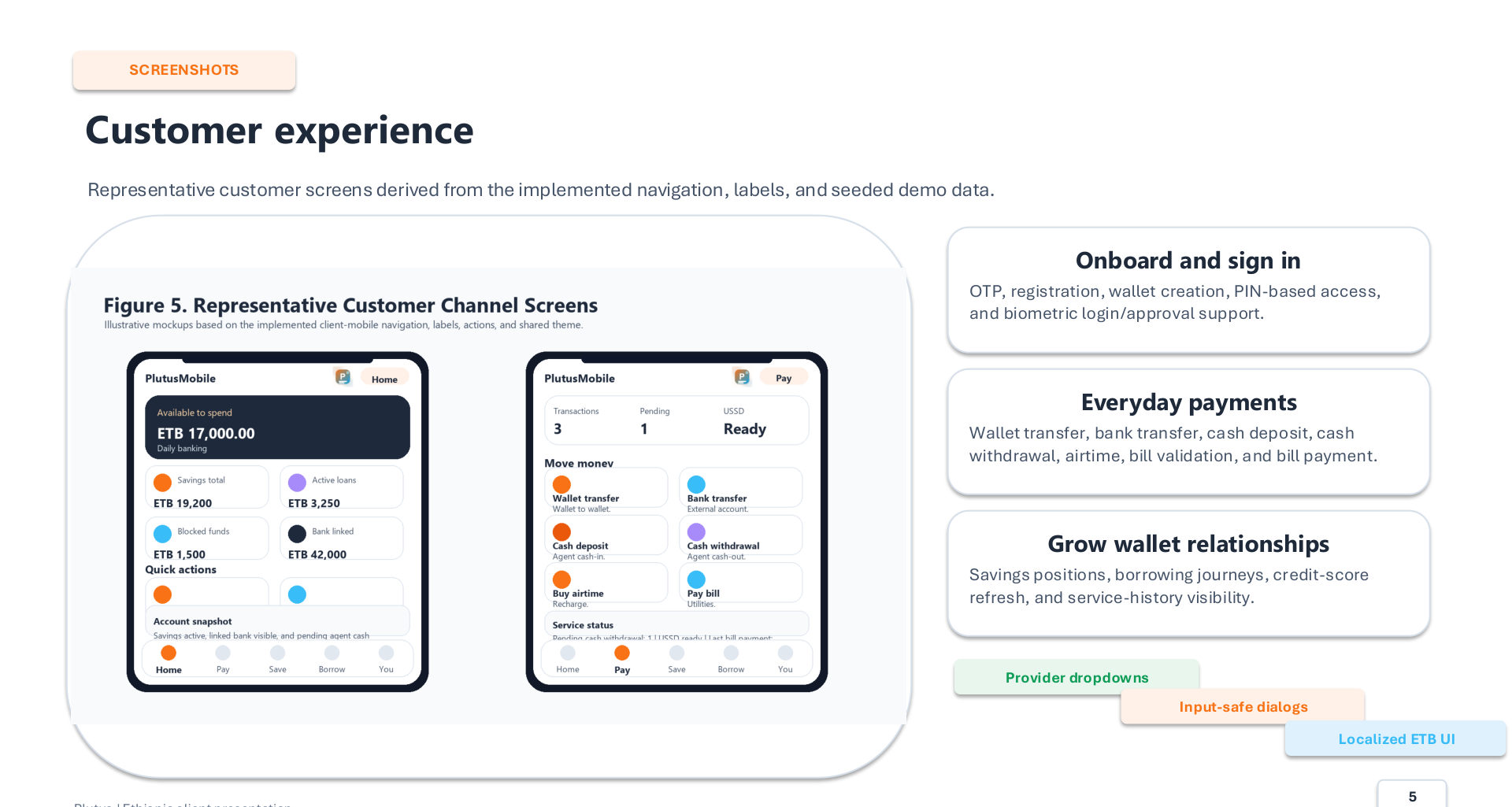

3. Customer experience was strong because the service model was broad from the start.

The customer side of the platform already covered the journeys that make a wallet commercially meaningful: onboarding, OTP-led registration, wallet creation, transfers, cash deposit and withdrawal requests, airtime, bill validation, bill payment, savings visibility, loan eligibility, borrowing journeys, and history.

That breadth matters. A wallet becomes strategically useful when it helps the institution deepen the relationship, not when it merely digitizes one isolated payment action. Plutus already reflected that wider relationship model.

The strongest wallet is not just a payment tool. It is a daily-use financial relationship built into one service platform.

Digital finance success principle

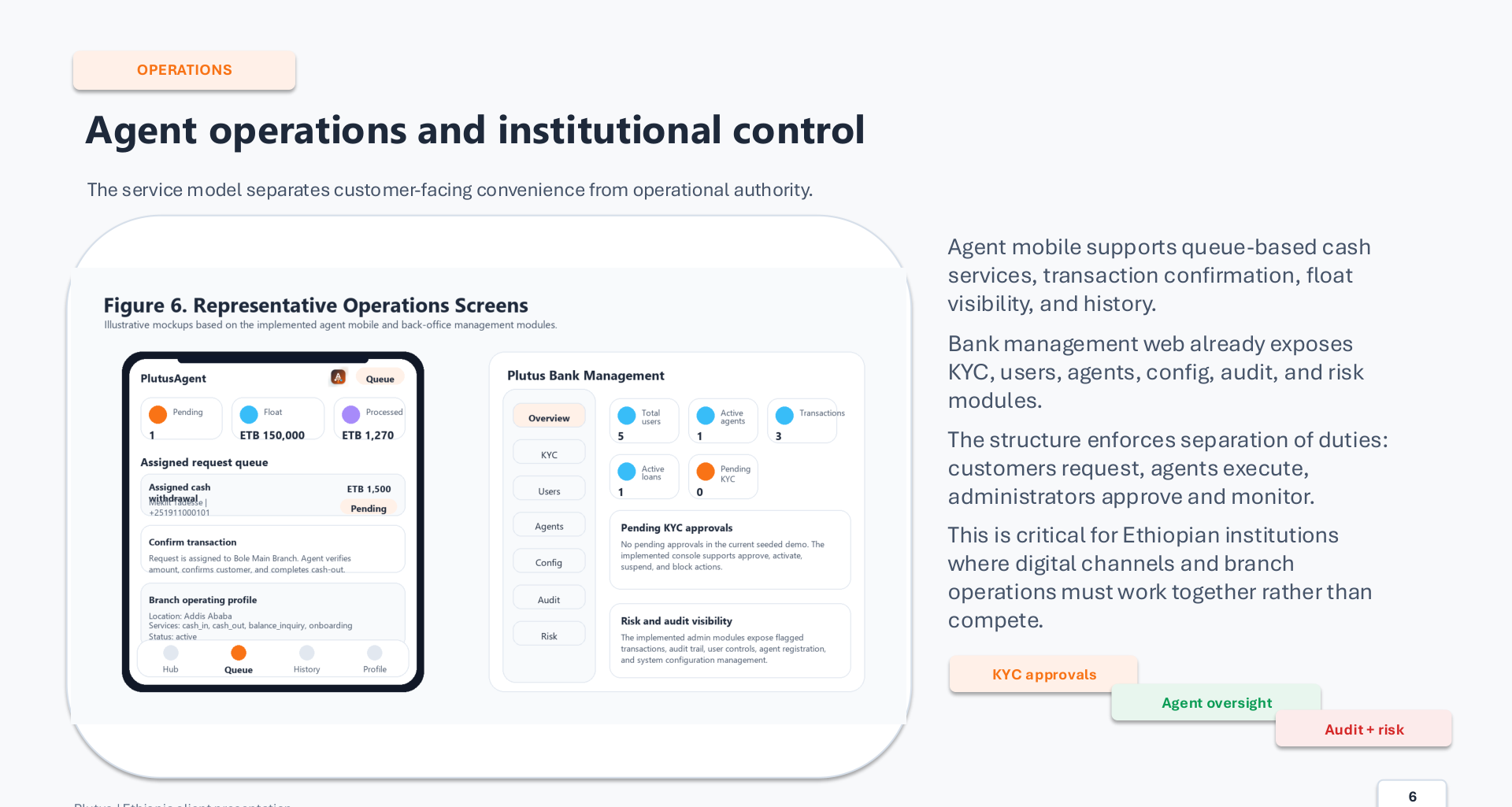

4. The operational story was even stronger because control was designed in, not added later.

Many digital-channel projects look polished on the customer side but feel weak once operational authority, approvals, and branch reality enter the picture. Plutus avoided that trap. It separated customer convenience from institutional authority clearly: customers request, agents execute cash services, and administrators approve, configure, and monitor.

That is exactly the structure an Ethiopian bank or MFI needs when branch operations and digital channels must work together rather than compete with each other.

- Agent operations: queue-based cash handling, confirmations, float visibility, and history.

- Back-office control: KYC review, user status control, agent oversight, configuration management, audit, and risk visibility.

- Governance strength: a visible separation of duties that made the platform easier to trust and easier to scale.

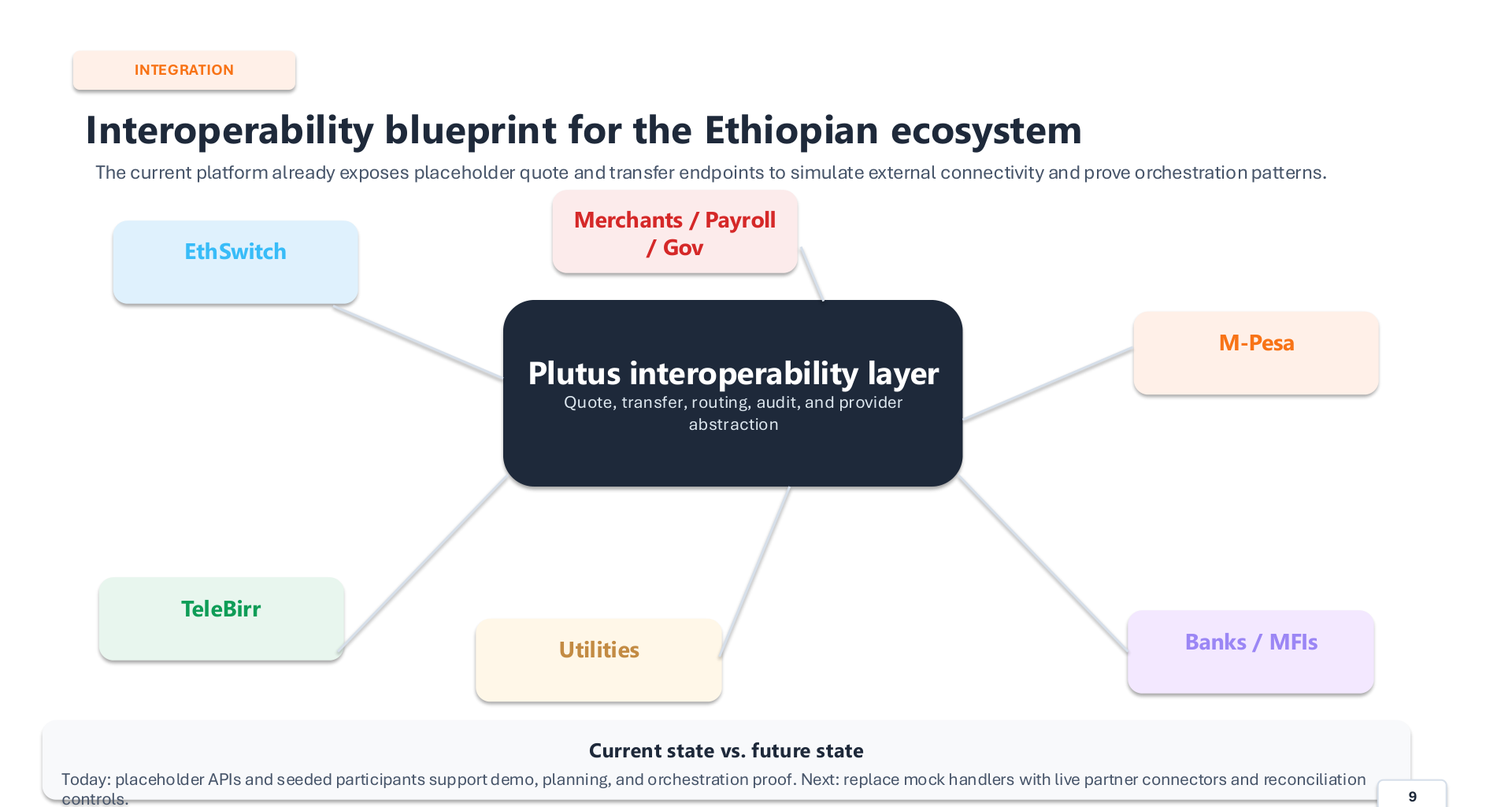

5. Interoperability was treated as a growth path, not a future excuse.

One of the most commercially important parts of the story was that Plutus already showed where the ecosystem was heading. Placeholder quote and transfer endpoints made it possible to demonstrate orchestration patterns for EthSwitch, TeleBirr, M-Pesa, banks, MFIs, utilities, and merchant or payroll use cases without pretending that every live connector had already been completed.

That honesty improved the story rather than weakening it. Clients could see both what was already real and what the production integration path would require next.

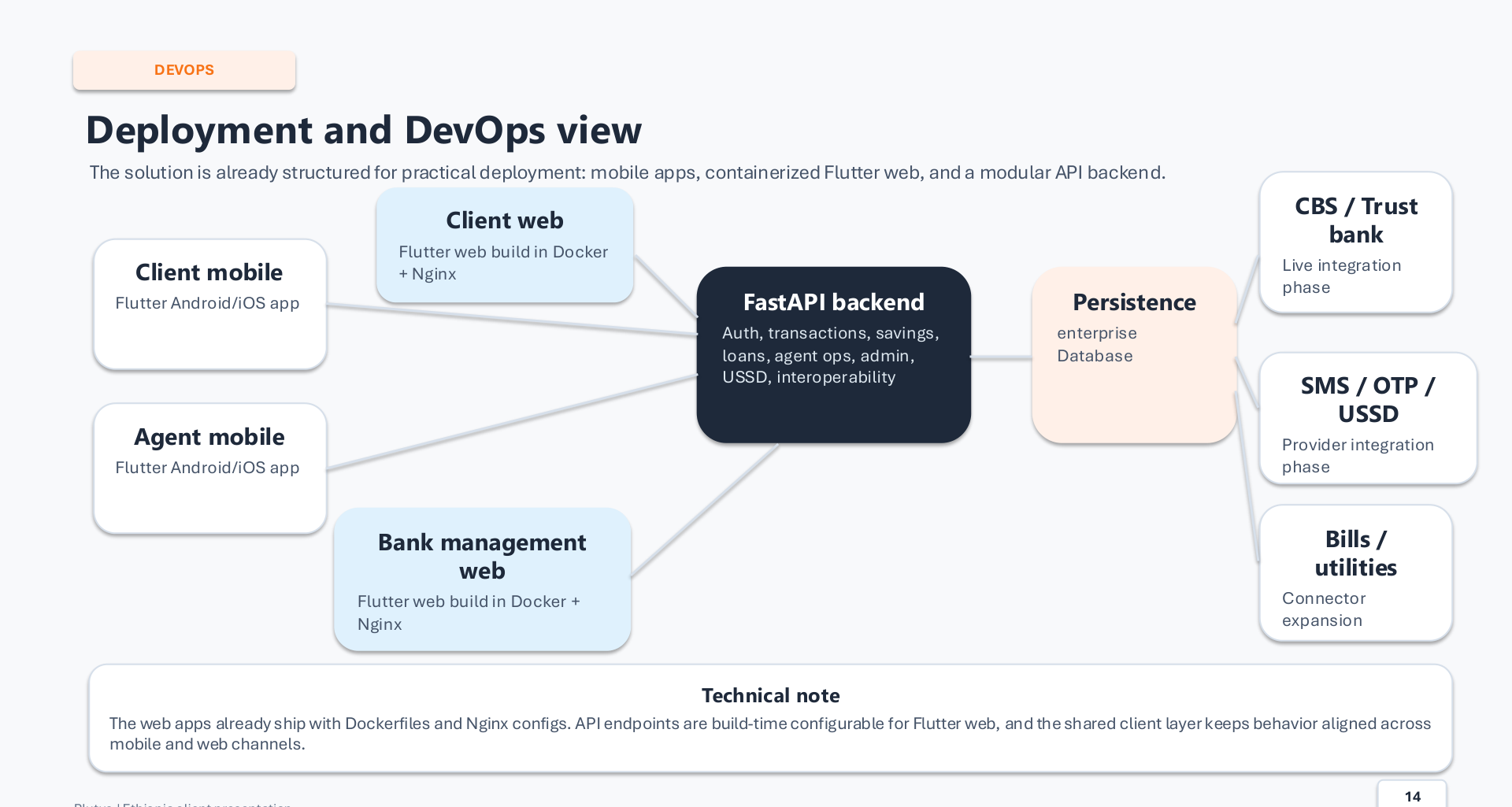

6. The platform also looked ready for deployment, not just demonstration.

Another reason the story worked is that the technical posture was already practical. Mobile apps, containerized Flutter web applications, and a modular FastAPI backend gave the client a deployment picture that felt operationally real. The web applications already had Docker and Nginx patterns. Shared client logic already aligned behavior across mobile and web. The backend was already organized around modular service domains.

That matters because leadership confidence drops quickly when a digital product looks polished but the delivery model still feels improvised. Plutus did not have that problem.

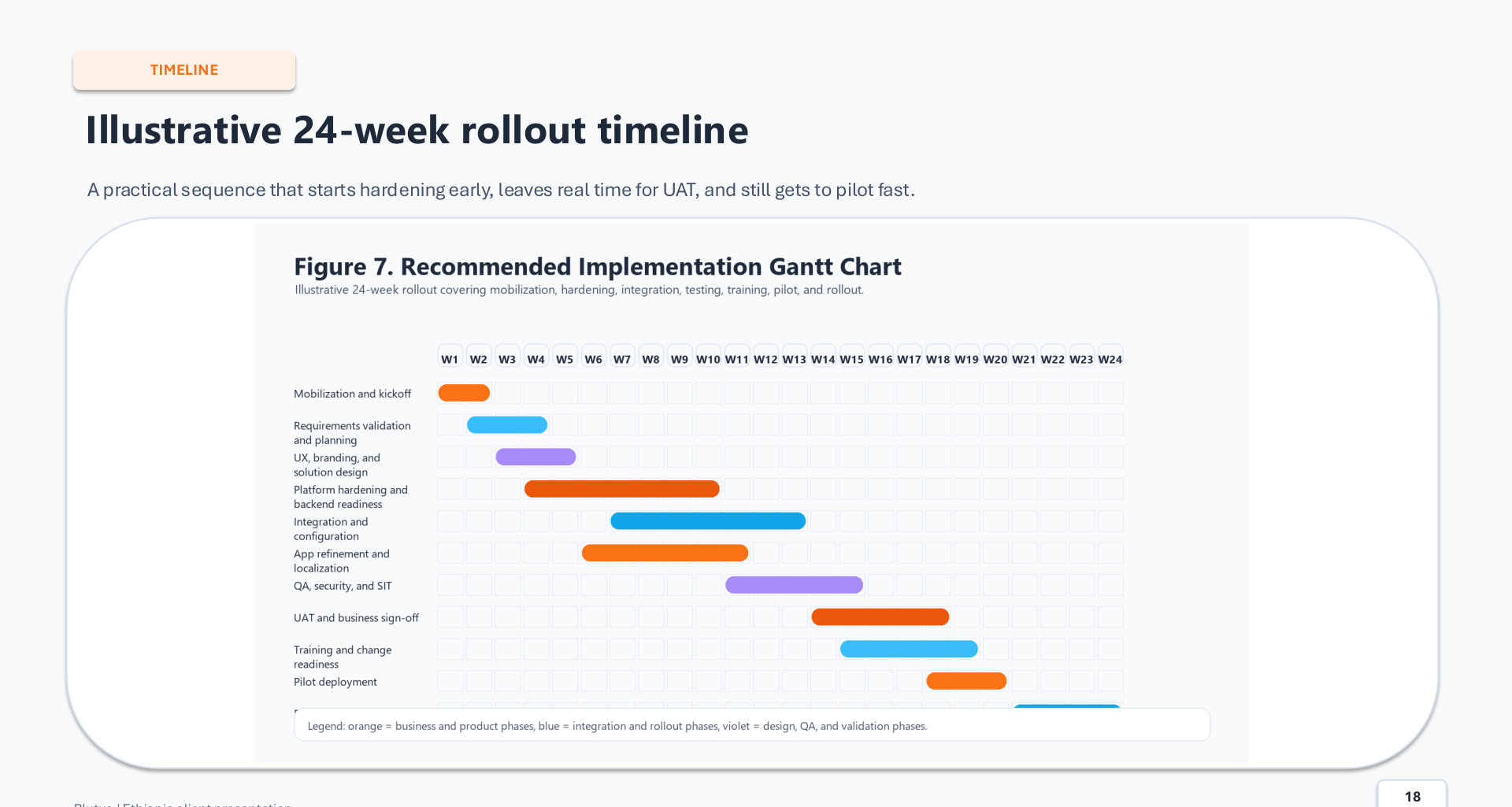

7. The final breakthrough was that rollout itself was already thinkable.

The strongest success stories do not end with “the product exists.” They end with “the path to pilot is clear.” Plutus had that advantage. The implementation workstreams were already understandable: mobilization, hardening, integration, channel refinement, data and reporting, QA, training and readiness, then pilot and hypercare.

That made the programme easier to govern. Stage gates were visible. Roles were visible. A 24-week timeline was visible. The project no longer had to be explained as a leap of faith.

What the success really was

The real success was that Plutus transformed a risky “build it from scratch” conversation into a controlled “harden it, integrate it, pilot it, and scale it” conversation. That is a very different executive decision.

The executive takeaway

Plutus succeeded because it made digital-wallet transformation feel practical. Customer journeys were already present. Agent and branch operations were already present. Controls were already present. The interoperability direction was already visible. The deployment model was already credible. And the path to pilot was already governable.

For Ethiopian institutions, that is what a strong success story looks like: not a concept that might one day become real, but a real foundation that makes the next phase of work faster, safer, and easier to approve.

What happens next

- Confirm the delivered platform as the base for the digital wallet and agency banking programme.

- Baseline integrations, branding, hosting, controls evidence, and success measures with business and technology stakeholders.

- Execute the hardening, integration, UAT, training, and controlled pilot path before wider scale-out.